I often talk about the 61 repeatable forms of gameplay in the market and I know I'm a bit behind on doing those posts. I don't normally stray off the path but I thought I'd cover a well known game called last man standing. The reason why I want to talk about this, is there seems to be continued misunderstanding about Amazon and what's likely to happen. Now there are two possible reasons - either I'm wrong or lots of other people are.

Hence, I'll put my stall forward.

Amazon is likely to be supply constrained when it comes to AWS and EC2. What I mean by this is that it takes time, money and resources to build data centres. You can't magic them out of the air. With AWS already doubling in physical size (or close to) each year, this creates considerable pressure and if AWS were to drop the price too quickly then demand will go up to outstrip supply (i.e. it just won't be able to build data centres fast enough). Hence Amazon would have to control pricing in order to control demand.

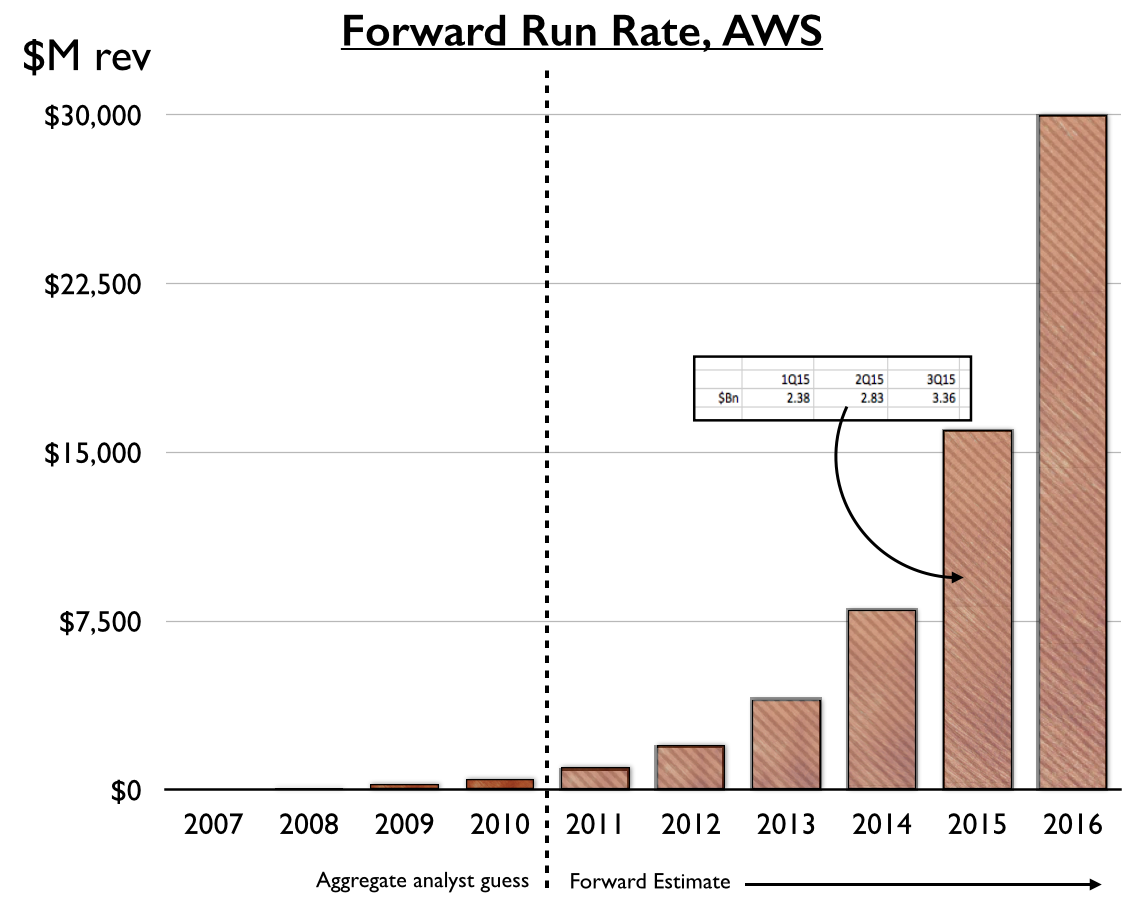

I know that people talk about AWS being a low margin business but I'll stick with older figures and say that Amazon is probably making a gross (not net) margin of 80%+. Let us look at revenue and for this, I'll turn to an old model from my Canonical days (see figure 1) after which we will cover a couple of key points in time that are coming up in that model.

I know that people talk about AWS being a low margin business but I'll stick with older figures and say that Amazon is probably making a gross (not net) margin of 80%+. Let us look at revenue and for this, I'll turn to an old model from my Canonical days (see figure 1) after which we will cover a couple of key points in time that are coming up in that model.

Figure 1 - Estimated of Forward Revenue Run rate.

By my past reckoning then by 2014, AWS would have a forward run rate of around $8Bn. Which means in 2015, it would make around $8Bn or more in revenue. Currently people are estimating at around $5-6Bn, so I count that as pretty damn good to get into the right order of magnitude. However, this is not about how accurate or inaccurate I might have been. This is about the steps and what roughly will happen.

1) In 2015, I expected AWS to clock a revenue of $8Bn+, a gross margin of 80%+, for Amazon still to be supply constrained and for a few examples of some large companies reliant on cloud (i.e. what we now call data centre zero companies)

2) In 2016, I expected AWS to clock a revenue of $16Bn+, a gross margin near to 80%, for Amazon still to be supply constrained, a very visible movement of companies towards using AWS and the market around AWS skills to heat up. I expected by the end of the year for the wheels to start coming off the whole private cloud market (which is why I've warned about this being the crunch time).

3) In 2017, I expected AWS to clock a revenue of $30 Bn+, a gross margin near to 80% and Amazon still to have to control pricing. However, by the end of the year I expected this supply tension to reduce as the growth rate would show signs of levelling. This will provide more opportunity to reduce pricing to keep physical growth to doubling. I expect AWS skills to be reaching fever pitch and the wheels to be flying off the private cloud market.

4) In 2018, I expected AWS to clock a revenue of $50Bn+. I expected gross margin (and prices) to start coming down fairly rapidly as Amazon has significantly more price freedom (i.e. is far less price constrained than is currently the case). Data centre zero companies will become prevalent and there will still be a fever pitch around AWS skills.

5) In 2019, I expected AWS prices to be rapidly dropping, the growth rates to continue levelling, the fall-out to start biting into hardware competitors, the private cloud industry to have practically vanished and the remaining laggards to be making a desperate dash into cloud.

6) By 2020, the game is not only all over (last chance saloon was back in 2012) but we start chalking up the casualties.

This doesn't mean there won't be niches - there will be and it's in these spaces that some open source efforts will hopefully hide out for future battles. This doesn't mean that some geographic regions won't try and hold out for spurious reasons - they will and at the same time harm their own competitive industries. This doesn't even mean I think my own figures or timing will be right, remember this model is ages old. I'm no fortune teller and at best I view it as being in the right direction. However, until someone gives me a better direction then this is the one that I've stuck with and so far, it seems to be fairly close.

Oh, and the last man standing? Well, in the last few years of the model when the price is dropping then it is all about last man standing. Many competitors won't be in a position to cope with how low the prices will go. The economies of scale will start to really tell here. Many will fall and it won't be gentle and graceful like. It'll be more brick like as in brick fired from a howitzer pointing downwards on the top of a building.

P.S. Before someone tells me the big hardware vendors are going to make a difference in infrastructure ... please don't. It's over. It has been over for sometime. Even if I had $50 Bn, I need to build the system, build the team, build the data centres before I launched and at any reasonable scale (even with using acquisition as a short cut) I'd be talking two years+ at lightning fast speed. I'd be walking into this market as a well funded startup against a massive behemoth who owned the ecosystem. Even those ex-hardware vendors with existing cloud efforts have too little, too late. No amount of money is going to save them here. These companies are just going through the motions of hanging on for as long as they can. There's a platform play but that's a different post.

P.P.S There will be some cloud players left - AWS will dominate followed by MSFT and then Google and a player like Alibaba. There'll be some jostling for position and geographic advantages.

P.S. Before someone tells me the big hardware vendors are going to make a difference in infrastructure ... please don't. It's over. It has been over for sometime. Even if I had $50 Bn, I need to build the system, build the team, build the data centres before I launched and at any reasonable scale (even with using acquisition as a short cut) I'd be talking two years+ at lightning fast speed. I'd be walking into this market as a well funded startup against a massive behemoth who owned the ecosystem. Even those ex-hardware vendors with existing cloud efforts have too little, too late. No amount of money is going to save them here. These companies are just going through the motions of hanging on for as long as they can. There's a platform play but that's a different post.

P.P.S There will be some cloud players left - AWS will dominate followed by MSFT and then Google and a player like Alibaba. There'll be some jostling for position and geographic advantages.